Page 111 - Moreno Valley 2025 Annual Financial Report

P. 111

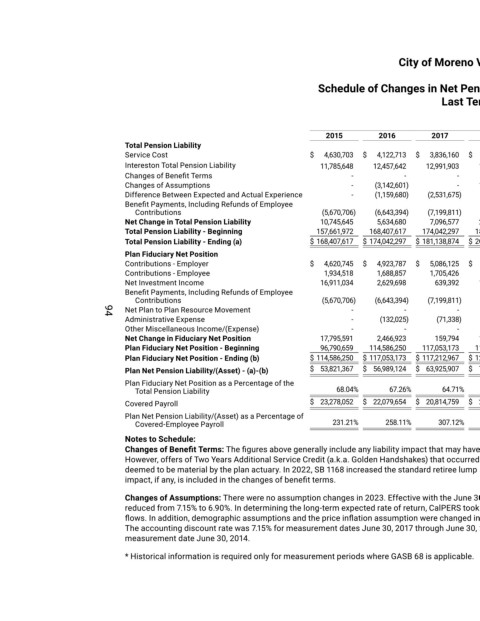

City of Moreno Valley, California

Schedule of Changes in Net Pension Liability and Related Ratios

Last Ten Years*

Measurement Period ended June 30

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Total Pension Liability

Service Cost $ 4,630,703 $ 4,122,713 $ 3,836,160 $ 4,154,188 $ 4,096,701 $ 4,421,787 $ 4,706,624 $ 4,410,902 $ 4,610,295 $ 4,769,622

Intereston Total Pension Liability 11,785,648 12,457,642 12,991,903 13,608,182 14,018,703 15,737,260 16,516,203 16,903,144 17,744,011 18,456,957

Changes of Benefit Terms - - - - - - - - 306,426 -

Changes of Assumptions - (3,142,601) - 11,559,898 (1,695,079) - - 8,512,485 - -

Difference Between Expected and Actual Experience - (1,159,680) (2,531,675) (566,196) (2,163,560) 1,544,561 876,743 (4,439,439) 2,841,506 1,422,588

Benefit Payments, Including Refunds of Employee

Contributions (5,670,706) (6,643,394) (7,199,811) (7,770,872) (8,495,988) (9,934,145) (10,633,661) (11,707,851) (13,042,533) (14,005,505)

Net Change in Total Pension Liability 10,745,645 5,634,680 7,096,577 20,985,200 5,760,777 11,769,463 11,465,909 13,679,241 12,459,705 10,643,662

Total Pension Liability - Beginning 157,661,972 168,407,617 174,042,297 181,138,874 202,124,074 221,313,159 233,082,622 244,548,531 258,227,772 270,687,477

Total Pension Liability - Ending (a) $ 168,407,617 $ 174,042,297 $ 181,138,874 $ 202,124,074 $ 207,884,851 $ 233,082,622 $ 244,548,531 $ 258,227,772 $ 270,687,477 $ 281,331,139

Plan Fiduciary Net Position

Contributions - Employer $ 4,620,745 $ 4,923,787 $ 5,086,125 $ 5,743,170 $ 6,385,610 $ 7,971,246 $ 8,002,625 $ 9,026,559 $ 10,016,695 $ 10,551,435

Contributions - Employee 1,934,518 1,688,857 1,705,426 1,676,844 1,721,640 1,801,643 1,414,837 1,659,557 1,787,788 2,308,151

Net Investment Income 16,911,034 2,629,698 639,392 13,032,362 11,053,578 7,444,800 35,531,661 (14,386,583) 10,916,480 17,788,583

Benefit Payments, Including Refunds of Employee

Contributions (5,670,706) (6,643,394) (7,199,811) (7,770,872) (8,495,988) (9,934,145) (10,633,661) (11,707,851) (13,042,533) (14,005,505)

Net Plan to Plan Resource Movement - - - (7,368) (323) - - - - -

Administrative Expense - (132,025) (71,338) (173,057) (202,130) (209,231) (155,326) (118,141) (128,043) (149,457)

94

Other Miscellaneous Income/(Expense) - - - - (383,849) - - - - -

Net Change in Fiduciary Net Position 17,795,591 2,466,923 159,794 12,501,079 10,078,538 7,074,313 34,160,136 (15,526,459) 9,550,387 16,493,207

Plan Fiduciary Net Position - Beginning 96,790,659 114,586,250 117,053,173 117,212,967 129,714,046 148,416,886 155,491,199 189,651,335 174,124,876 183,675,263

Plan Fiduciary Net Position - Ending (b) $ 114,586,250 $ 117,053,173 $ 117,212,967 $ 129,714,046 $ 139,792,584 $ 155,491,199 $ 189,651,335 $ 174,124,876 $ 183,675,263 $ 200,168,470

Plan Net Pension Liability/(Asset) - (a)-(b) $ 53,821,367 $ 56,989,124 $ 63,925,907 $ 72,410,028 $ 68,092,267 $ 77,591,423 $ 54,897,196 $ 84,102,896 $ 87,012,214 $ 81,162,669

Plan Fiduciary Net Position as a Percentage of the

Total Pension Liability 68.04% 67.26% 64.71% 64.18% 67.25% 66.71% 77.55% 67.43% 67.86% 71.15%

Covered Payroll $ 23,278,052 $ 22,079,654 $ 20,814,759 $ 20,793,815 $ 20,860,026 $ 23,174,982 $ 24,680,774 $ 21,728,582 $ 23,776,664 $ 25,343,369

Plan Net Pension Liability/(Asset) as a Percentage of

Covered-Employee Payroll 231.21% 258.11% 307.12% 348.23% 326.42% 334.81% 222.43% 387.06% 365.96% 320.25%

Notes to Schedule:

Changes of Benefit Terms: The figures above generally include any liability impact that may have resulted from voluntary benefit changes that occurred on or before the Measurement Date.

However, offers of Two Years Additional Service Credit (a.k.a. Golden Handshakes) that occurred after the Valuation Date are not included in the figures above, unless the liability impact is

deemed to be material by the plan actuary. In 2022, SB 1168 increased the standard retiree lump sum death benefit from $500 to $2,000 for any death occurring on or after July 1, 2023. The

impact, if any, is included in the changes of benefit terms.

Changes of Assumptions: There were no assumption changes in 2023. Effective with the June 30, 2021 valuation date (June 30, 2022 measurement date), the accounting discount rate was

reduced from 7.15% to 6.90%. In determining the long-term expected rate of return, CalPERS took into account long-term market return expectations as well as the expected pension fund cash

flows. In addition, demographic assumptions and the price inflation assumption were changed in accordance with the 2021 CalPERS Experience Study and Review of Actuarial Assumptions.

The accounting discount rate was 7.15% for measurement dates June 30, 2017 through June 30, 2021, 7.65% for measurement dates June 30, 2015 through June 30, 2016, and 7.50% for

measurement date June 30, 2014.

* Historical information is required only for measurement periods where GASB 68 is applicable.