Page 113 - Moreno Valley 2025 Annual Financial Report

P. 113

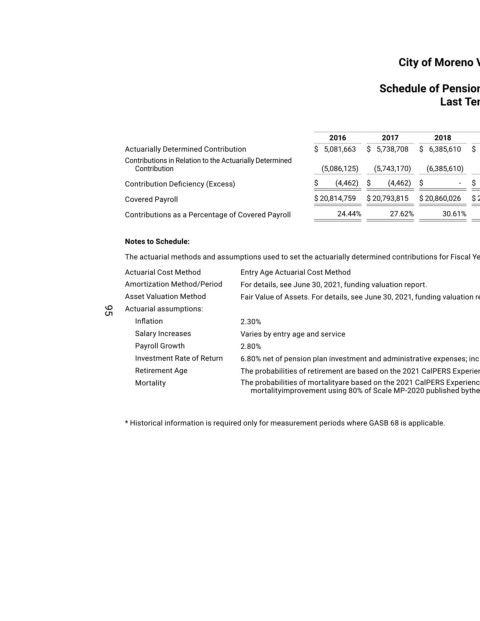

City of Moreno Valley, California

Schedule of Pension Plan Contributions

Last Ten Years*

For the Fiscal Years Ended June 30

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Actuarially Determined Contribution $ 5,081,663 $ 5,738,708 $ 6,385,610 $ 7,094,031 $ 7,971,246 $ 8,002,625 $ 9,026,559 $ 10,016,695 $ 10,551,435 $ 11,638,621

Contributions in Relation to the Actuarially Determined

Contribution (5,086,125) (5,743,170) (6,385,610) (7,094,031) (7,971,246) (8,002,625) (9,026,559) (10,016,695) (10,551,435) (11,638,621)

Contribution Deficiency (Excess) $ (4,462) $ (4,462) $ - $ - $ - $ - $ - $ - $ - $ -

Covered Payroll $ 20,814,759 $ 20,793,815 $ 20,860,026 $ 21,783,847 $ 23,174,982 $ 24,680,774 $ 21,728,582 $ 23,776,664 $ 25,343,369 $ 32,226,538

Contributions as a Percentage of Covered Payroll 24.44% 27.62% 30.61% 32.57% 34.40% 32.42% 41.54% 42.13% 41.63% 36.12%

Notes to Schedule:

The actuarial methods and assumptions used to set the actuarially determined contributions for Fiscal Year 2023-24 were derived from the June 30, 2021 funding valuation report.

Actuarial Cost Method Entry Age Actuarial Cost Method

Amortization Method/Period For details, see June 30, 2021, funding valuation report.

Asset Valuation Method Fair Value of Assets. For details, see June 30, 2021, funding valuation report.

Actuarial assumptions:

Inflation 2.30%

95

Salary Increases Varies by entry age and service

Payroll Growth 2.80%

Investment Rate of Return 6.80% net of pension plan investment and administrative expenses; includes inflation.

Retirement Age The probabilities of retirement are based on the 2021 CalPERS Experience Study and Review of Actuarial Assumptions.

Mortality The probabilities of mortalityare based on the 2021 CalPERS Experience Study and Review of Actuarial Assumptions. Mortality rates incorporate full generational

mortalityimprovement using 80% of Scale MP-2020 published bythe Society of Actuaries.

* Historical information is required only for measurement periods where GASB 68 is applicable.