Page 92 - Moreno Valley 2025 Annual Financial Report

P. 92

City of Moreno Valley, California

Notes to Financial Statements

For the Year Ended June 30, 2025

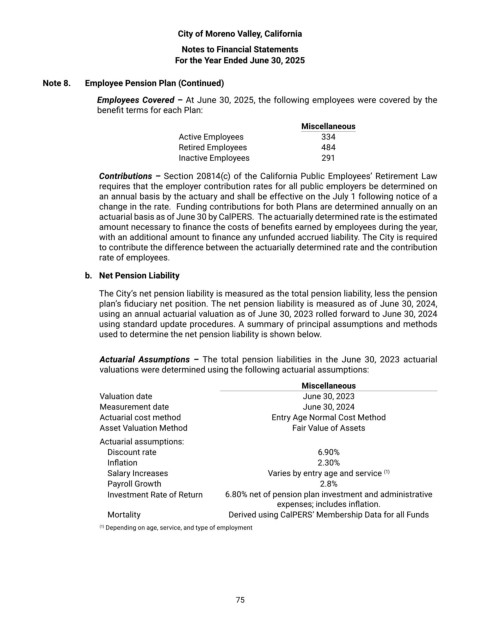

Note 8. Employee Pension Plan (Continued)

Employees Covered – At June 30, 2025, the following employees were covered by the

benefit terms for each Plan:

Miscellaneous

Active Employees 334

Retired Employees 484

Inactive Employees 291

Contributions – Section 20814(c) of the California Public Employees’ Retirement Law

requires that the employer contribution rates for all public employers be determined on

an annual basis by the actuary and shall be effective on the July 1 following notice of a

change in the rate. Funding contributions for both Plans are determined annually on an

actuarial basis as of June 30 by CalPERS. The actuarially determined rate is the estimated

amount necessary to finance the costs of benefits earned by employees during the year,

with an additional amount to finance any unfunded accrued liability. The City is required

to contribute the difference between the actuarially determined rate and the contribution

rate of employees.

b. Net Pension Liability

The City’s net pension liability is measured as the total pension liability, less the pension

plan’s fiduciary net position. The net pension liability is measured as of June 30, 2024,

using an annual actuarial valuation as of June 30, 2023 rolled forward to June 30, 2024

using standard update procedures. A summary of principal assumptions and methods

used to determine the net pension liability is shown below.

Actuarial Assumptions – The total pension liabilities in the June 30, 2023 actuarial

valuations were determined using the following actuarial assumptions:

Miscellaneous

Valuation date June 30, 2023

Measurement date June 30, 2024

Actuarial cost method Entry Age Normal Cost Method

Asset Valuation Method Fair Value of Assets

Actuarial assumptions:

Discount rate 6.90%

Inflation 2.30%

Salary Increases Varies by entry age and service (1)

Payroll Growth 2.8%

Investment Rate of Return 6.80% net of pension plan investment and administrative

expenses; includes inflation.

Mortality Derived using CalPERS’ Membership Data for all Funds

(1) Depending on age, service, and type of employment

75