Page 96 - Moreno Valley 2025 Annual Financial Report

P. 96

City of Moreno Valley, California

Notes to Financial Statements

For the Year Ended June 30, 2025

Note 8. Employee Pension Plan (Continued)

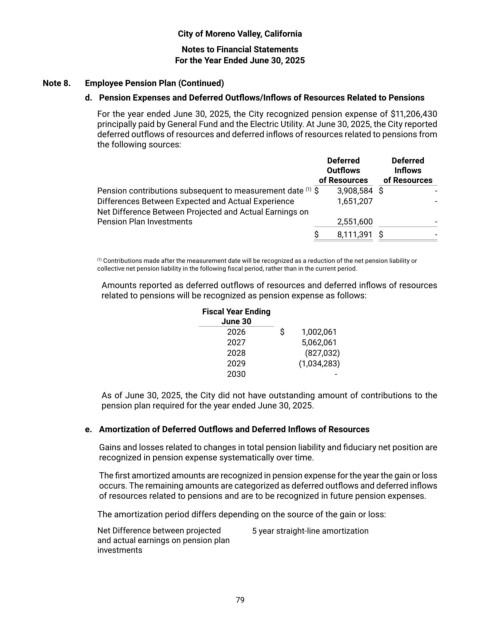

d. Pension Expenses and Deferred Outflows/Inflows of Resources Related to Pensions

For the year ended June 30, 2025, the City recognized pension expense of $11,206,430

principally paid by General Fund and the Electric Utility. At June 30, 2025, the City reported

deferred outflows of resources and deferred inflows of resources related to pensions from

the following sources:

Deferred Deferred

Outflows Inflows

of Resources of Resources

Pension contributions subsequent to measurement date (1) $ 3,908,584 $ -

Differences Between Expected and Actual Experience 1,651,207 -

Net Difference Between Projected and Actual Earnings on

Pension Plan Investments 2,551,600 -

$ 8,111,391 $ -

(1) Contributions made after the measurement date will be recognized as a reduction of the net pension liability or

collective net pension liability in the following fiscal period, rather than in the current period.

Amounts reported as deferred outflows of resources and deferred inflows of resources

related to pensions will be recognized as pension expense as follows:

Fiscal Year Ending

June 30

2026 $ 1,002,061

2027 5,062,061

2028 (827,032)

2029 (1,034,283)

2030 -

As of June 30, 2025, the City did not have outstanding amount of contributions to the

pension plan required for the year ended June 30, 2025.

e. Amortization of Deferred Outflows and Deferred Inflows of Resources

Gains and losses related to changes in total pension liability and fiduciary net position are

recognized in pension expense systematically over time.

The first amortized amounts are recognized in pension expense for the year the gain or loss

occurs. The remaining amounts are categorized as deferred outflows and deferred inflows

of resources related to pensions and are to be recognized in future pension expenses.

The amortization period differs depending on the source of the gain or loss:

Net Difference between projected 5 year straight-line amortization

and actual earnings on pension plan

investments

79