Page 44 - Moreno Valley 2025 Annual Financial Report

P. 44

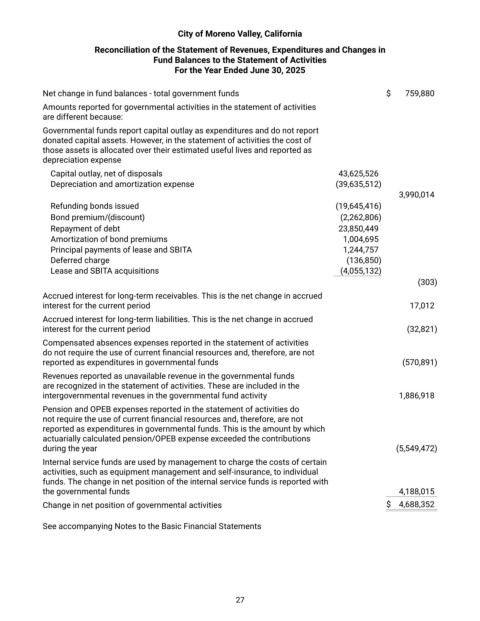

City of Moreno Valley, California

Reconciliation of the Statement of Revenues, Expenditures and Changes in

Fund Balances to the Statement of Activities

For the Year Ended June 30, 2025

Net change in fund balances ‐ total government funds $ 759,880

Amounts reported for governmental activities in the statement of activities

are different because:

Governmental funds report capital outlay as expenditures and do not report

donated capital assets. However, in the statement of activities the cost of

those assets is allocated over their estimated useful lives and reported as

depreciation expense

Capital outlay, net of disposals 43,625,526

Depreciation and amortization expense (39,635,512)

3,990,014

Refunding bonds issued (19,645,416)

Bond premium/(discount) (2,262,806)

Repayment of debt 23,850,449

Amortization of bond premiums 1,004,695

Principal payments of lease and SBITA 1,244,757

Deferred charge (136,850)

Lease and SBITA acquisitions (4,055,132)

(303)

Accrued interest for long‐term receivables. This is the net change in accrued

interest for the current period 17,012

Accrued interest for long‐term liabilities. This is the net change in accrued

interest for the current period (32,821)

Compensated absences expenses reported in the statement of activities

do not require the use of current financial resources and, therefore, are not

reported as expenditures in governmental funds (570,891)

Revenues reported as unavailable revenue in the governmental funds

are recognized in the statement of activities. These are included in the

intergovernmental revenues in the governmental fund activity 1,886,918

Pension and OPEB expenses reported in the statement of activities do

not require the use of current financial resources and, therefore, are not

reported as expenditures in governmental funds. This is the amount by which

actuarially calculated pension/OPEB expense exceeded the contributions

during the year (5,549,472)

Internal service funds are used by management to charge the costs of certain

activities, such as equipment management and self‐insurance, to individual

funds. The change in net position of the internal service funds is reported with

the governmental funds 4,188,015

Change in net position of governmental activities $ 4,688,352

See accompanying Notes to the Basic Financial Statements

27